Key Figures and Discoveries:

- 70% of Bitcoin’s circulating supply represents free float, potentially mitigating supply shock risks.

- The 1.75 million BTC decrease in LTH supply in 2024 indicates that there is still ample room for LTH selling pressure.

- U.S. spot ETFs absorbed 2.4x the annual mining supply in 2024, but their trading volume represents less than 4% of the market.

- MicroStrategy’s Bitcoin accumulation exceeded half the scale of net ETF inflows.

- Exchange reserves dropped by 21%, while OTC balance increased by 105%, hinting at supply redistribution.

- Around 40% of Bitcoin’s transaction volume in 2024 was linked to exchanges.

- Bitcoin’s USD-denominated 2% market depth increased by 61%, suggesting an improved liquidity landscape.

- CEX.IO quadrupled its market share in 2024, becoming a top 2 exchange in terms of Bitcoin market depth.

Introduction

Bitcoin demonstrated remarkable performance in 2024, recording a more than 121% price increase and registering rising market dominance. The major catalyst behind this move was a supply-and-demand rebalance due to Bitcoin’s halving and the introduction of U.S. spot Bitcoin ETFs.

With Bitcoin’s continued expansion into traditional finance and the anticipation of a potential U.S. Bitcoin strategic reserve, some speculate that Bitcoin could face a significant supply shock in this cycle. These predictions even suggest Bitcoin could challenge the 4-year cycle theory, with its price growing at an unprecedented pace. While such claims arise every cycle, we decided to evaluate Bitcoin’s supply and liquidity landscape to understand its potential risks and opportunities.

Methodology

Our research employed the following resources to provide a holistic view of Bitcoin’s supply and liquidity:&

- Kaiko: To analyze aggregated market depth data and liquidity trends across over 30 major exchanges.

- CryptoQuant: To track flows between crypto platforms, including deposits and withdrawals, and their implications for market sentiment.

- Checkonchain: To assess supply dynamics and on-chain wallet behavior.

- Velo: To analyze cash-and-carry trade efficiency on the Bitcoin ETF market.

Long-Term Holder Supply Developments

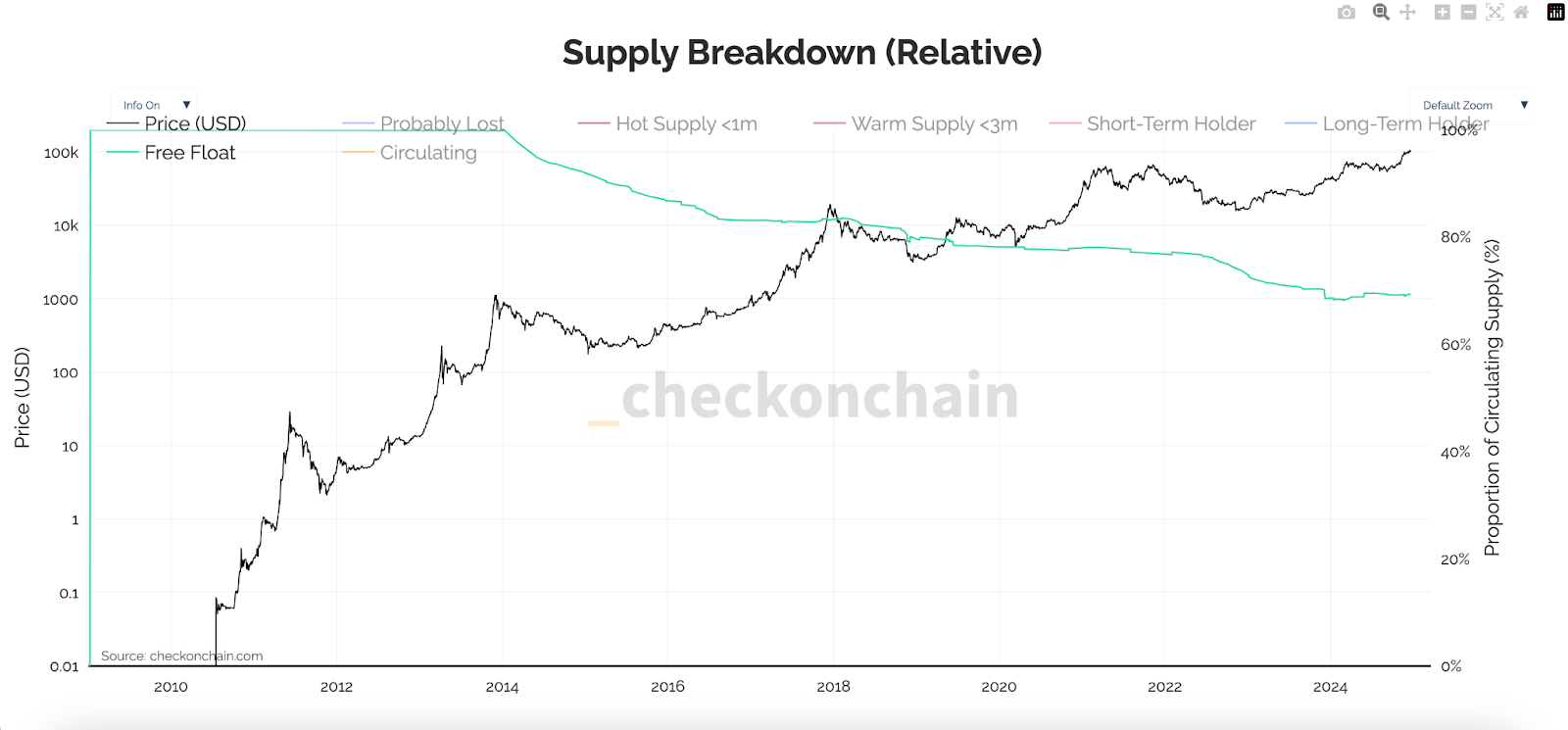

Free Float

By assessing the free float supply — the portion of coins potentially available for trading if their owners choose to sell — a clear decreasing trend emerges across cycles. This suggests that an increasing amount of Bitcoin becomes inactive, as more users HODL their coins for extended periods or probably lose access to their wallets, leading to concerns about a potential supply shock. However, the free float supply still represents 70% of the circulating supply, or over 13.76 million BTC, offering a massive potential to enhance existing Bitcoin liquidity.

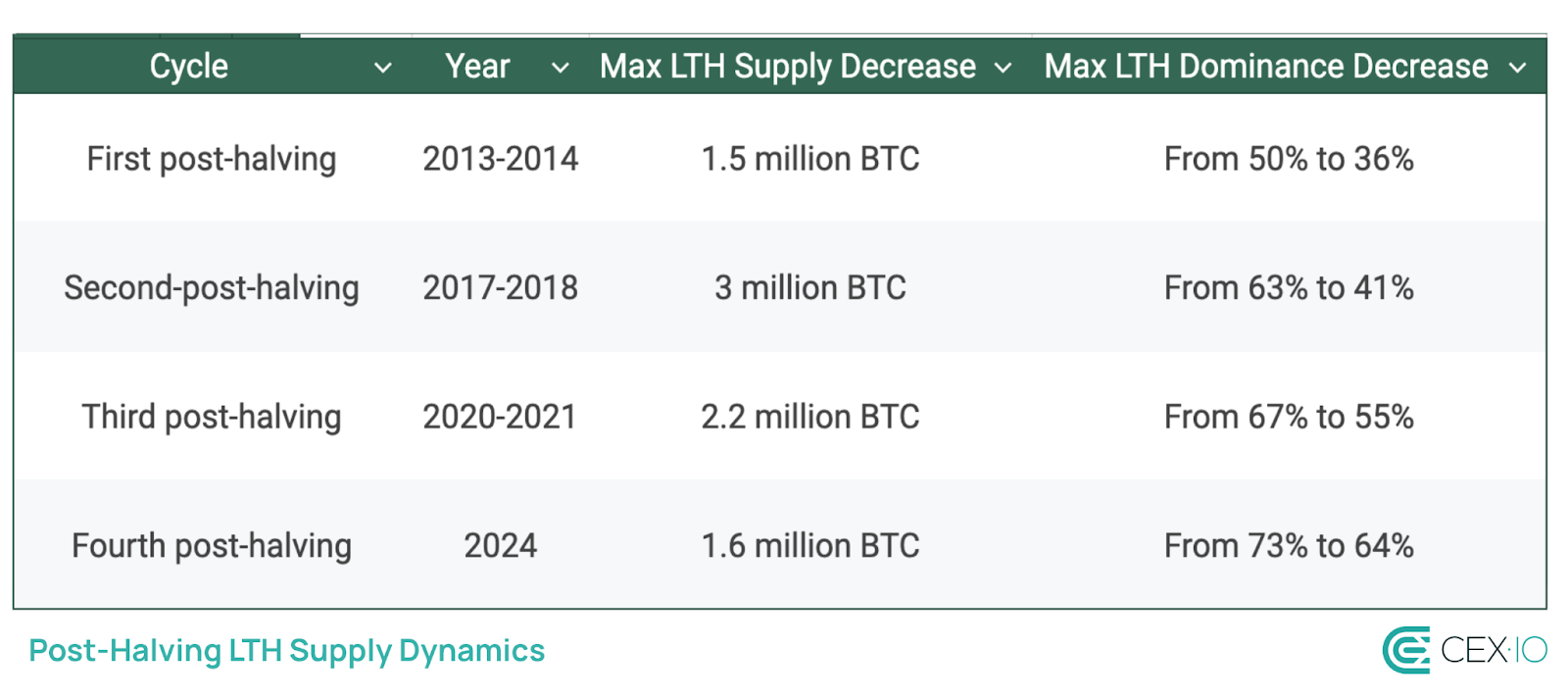

Post-Halving Behavior

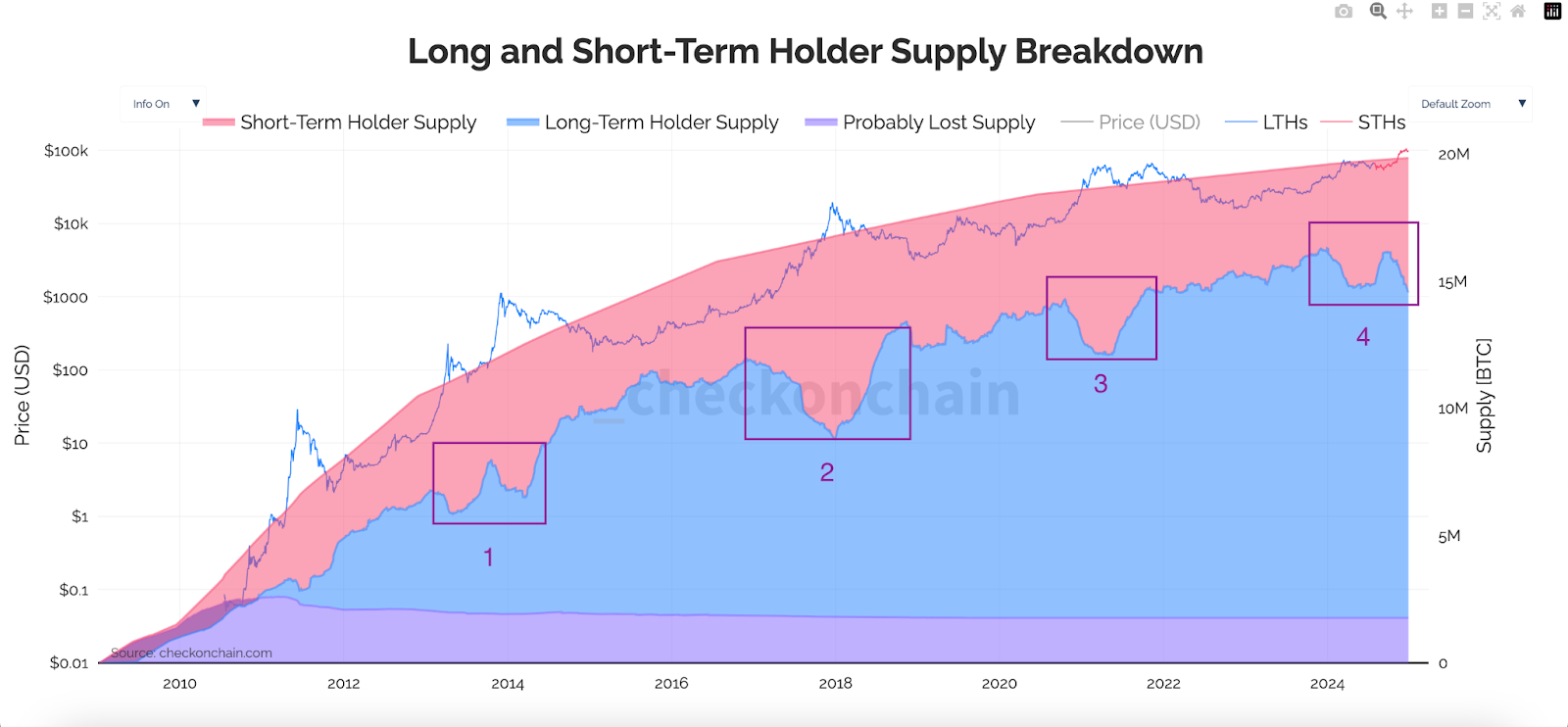

The decrease in free float supply is partly associated with long-term holder (LTH) supply, whose dominance increases with consecutive cycles. However, a notable portion of LTH supply becomes active post-halving, causing a briefly increased transition of coins to short-term holders (STH). Historically, such periods of decreased LTH dominance coincided with bull runs, heightened trading volumes, and improved market liquidity.&

In 2024, the LTH supply decreased by over 1.75 million BTC, now representing 64.4% of the circulating supply. A distinctive feature of this cycle was a sharp dip in LTH supply shortly before the halving, driven by Bitcoin’s unprecedented breakout to a new all-time high. While this decline had stabilized by September, a renewed LTH supply drop emerged in Q4, totaling 1.58 million BTC.

On average, the LTH supply has been losing around 16% in dominance during post-halving rallies. Considering the existing 9% post-halving decline in dominance, there is still ample room for LTH selling pressure in this cycle, which will likely be absorbed by newly joined market participants.

Note: Numbers represent the post-halving period highlighted in the table above.

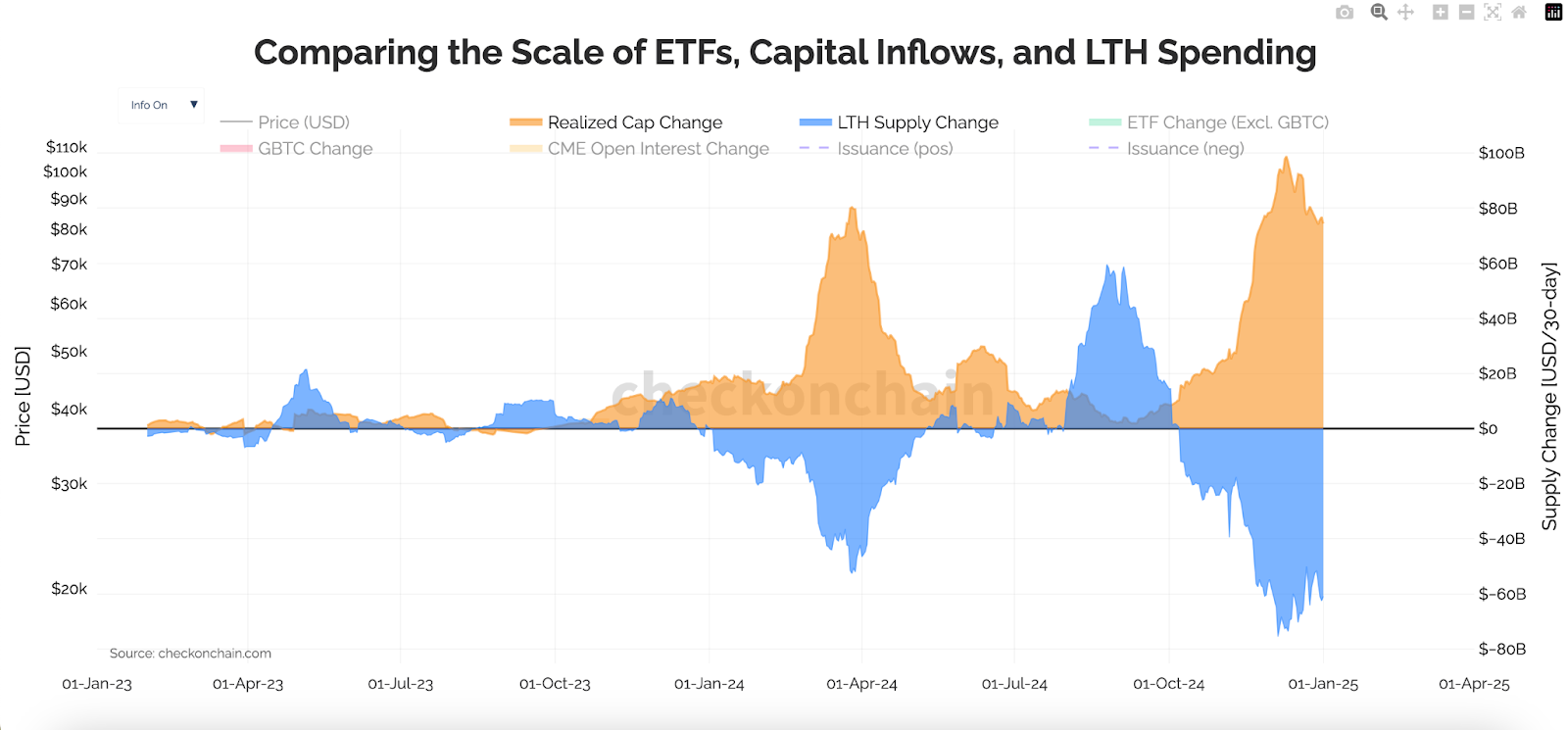

Most of the LTH selling pressure typically occurs during periods of significant increases in the realized cap. For example, in Q1 2024, a surge of up to $80 billion in the realized cap coincided with a $50 billion decline in LTH supply. This trend escalated in Q4, driving over $75 billion in LTH selling activity alongside a $90 billion increase in the realized cap. Such market behavior serves as a natural counterbalance to Bitcoin rallies, tempering upward momentum and contributing to the formation of local peaks, including 4-year cycle highs.

Looking into 2025

Any potential increase in demand from institutional investors and/or governments in 2025 will likely be met with a considerable increase in LTH profit-taking, pushing the LTH supply lower this year. Taking into account an average decline in LTH supply dominance during post-halving rallies, 1.4 million BTC could be potentially transferred from LTH to STH hands within 2025 bull run, enhancing market liquidity and mitigating the risks of a potential supply shock in this cycle.

ETF Market Dynamics

Rapid Adoption with Exaggerated Narratives

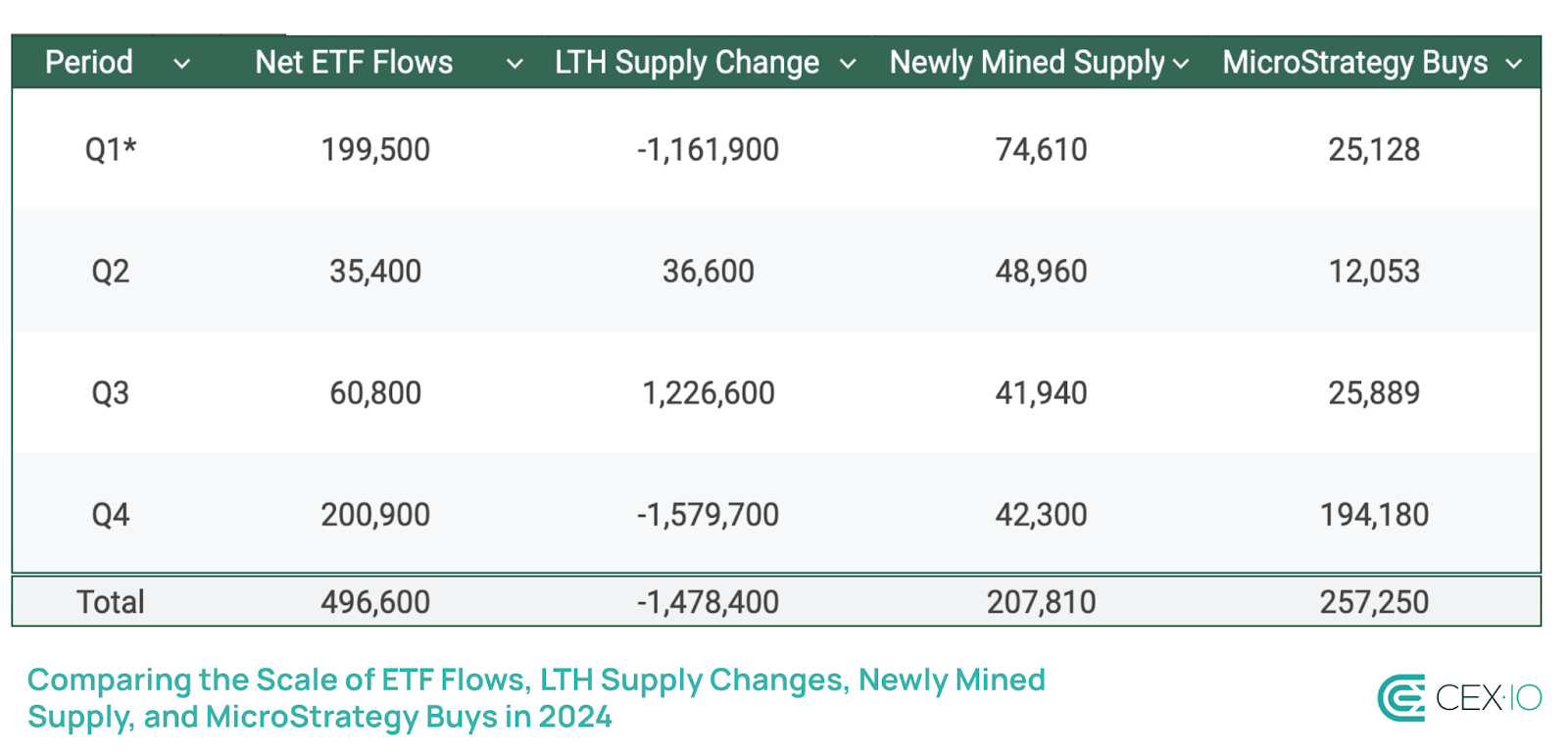

U.S. spot Bitcoin ETFs proved highly successful, accumulating around 500,000 BTC in 2024, and now collectively holding over 1.13 million BTC, or roughly 5.7% of Bitcoin’s circulating supply. This rapid adoption, bolstered by widespread reporting in both mainstream and industry media, raised concerns about a potential supply shock caused by ETFs. In most cases, these narratives compare ETF flows to the newly mined Bitcoin supply, particularly during days of significant inflows. However, a broader perspective reveals that while ETFs are influential, their impact may not be as substantial as often perceived.&

*Q1 performance includes data starting from January 11, 2024, when U.S. spot Bitcoin ETFs began available for trading. The data points are reflected in the amount of BTC over the selected period.

In 2024, net ETF flows outpaced the newly mined Bitcoin supply by approximately 2.4 times. Despite this outperformance, the trend has not been consistent. Notably, net ETF inflows lagged in Q2, even as the Bitcoin halving event significantly reduced the newly mined supply.

If compared to LTH supply dynamics, the weight of ETFs is falling even further. ETFs absorbed at most 35% of LTH supply, primarily in Q1 and Q4. This indicates that other factors, such as direct institutional buying or other non-ETF inflows, potentially played a more significant role in offsetting selling pressure directly. One notable factor has been MicroStrategy, which accumulated over 257,000 BTC in 2024 — an amount exceeding half the scale of net ETF inflows. It is worth noting, however, that MicroStrategy employs a TWAP strategy to minimize its market impact during Bitcoin purchases, meaning their accumulation has had a more subdued influence on price volatility compared to immediate large-volume trades.

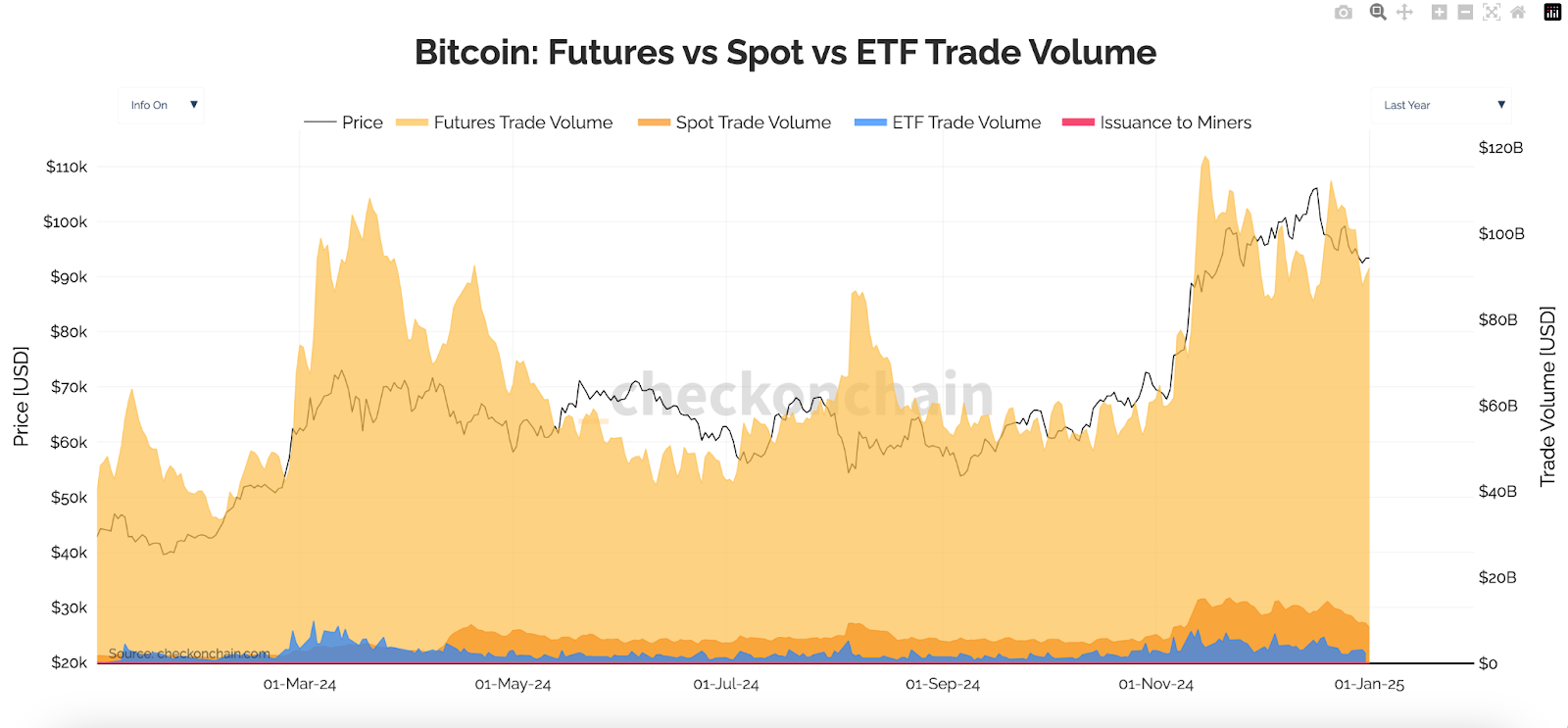

In addition, ETFs currently account for less than 4% of Bitcoin’s total trading volume. Although Q1 saw ETFs’ volume briefly surpass spot market volume, they now contribute about half of it.&

Impact of Cash-and-Carry Trade

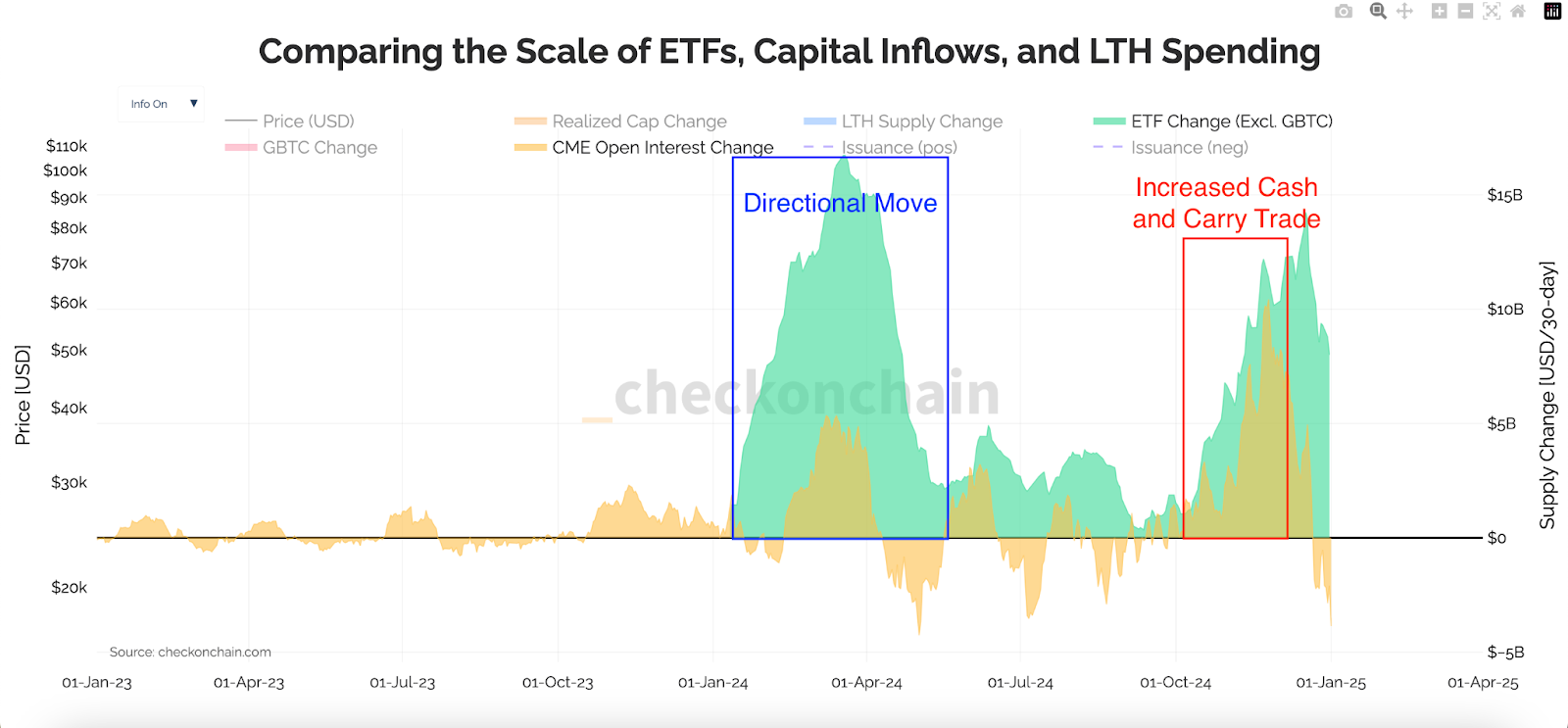

A substantial portion of ETF inflows in 2024 was driven by the cash-and-carry trade, not only directional investment. This arbitrage strategy involves buying ETFs while shorting Bitcoin futures, capturing the premium between the spot/ETF and futures prices. Since this is a market-neutral trade, which balances supply and demand, it does not exert directional pressure on Bitcoin prices.

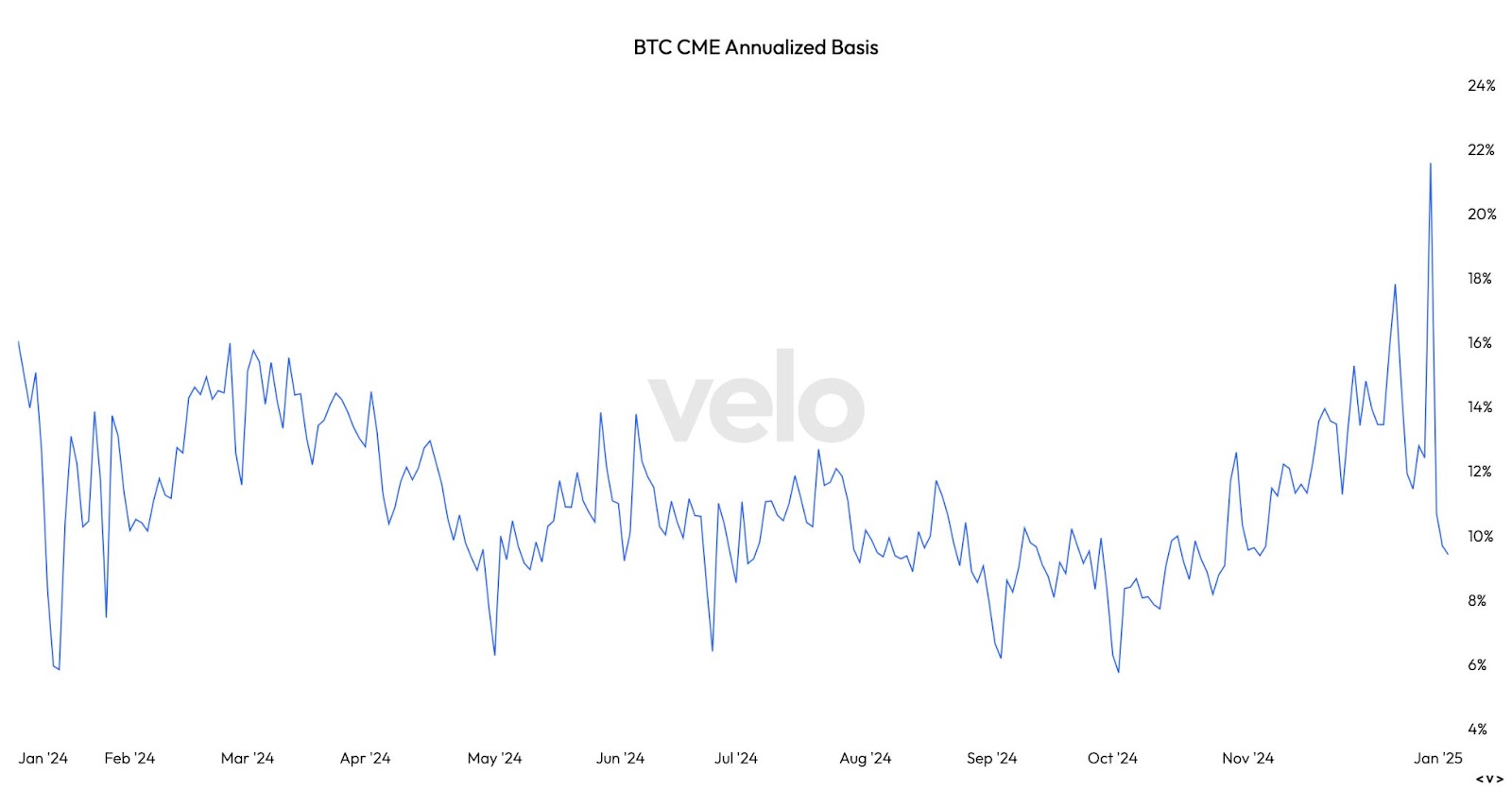

In 2024, cash-and-carry trade related to Bitcoin ETFs was typically executed using short positions on CME Bitcoin futures. According to Velo data, the annualized three-month basis in CME’s BTC futures has primarily been in the 5-15% range over the past year. In other words, setting up a cash-and-carry trade would earn investors 5-15%.&

Although 5-15% might not sound like much compared to Bitcoin’s 121% annual growth, it was enough to take advantage of this market inefficiency. By comparing the scale of ETF inflows and CME open interest, it can be seen that ETF activity in Q1 2024 was more directional, reflecting increased interest in Bitcoin exposure. Post-election, the market primarily shifted towards cash-and-carry trades, while in December, directional activity resurged, signaling renewed investor interest in outright Bitcoin exposure.

Looking into 2025

The recent introduction of ETF options could transform cash-and-carry trades in 2025 by offering a more flexible and precise hedging mechanism. While CME futures have traditionally been used for such strategies, ETF options provide an alternative that may reduce reliance on futures. This shift could also mitigate the risk of a Bitcoin supply shock, as these trades utilize derivatives without directly impacting the spot supply.

In this case, ETF flows would appear more like directional investments and may even ramp up, especially as Bitcoin’s post-halving rally seems far from conclusion. However, considering the existing pace, ETF-related activity currently appears insufficient to drive a potential supply shock and rather offsets the decline in native retail activity.

Reserves on Trading Platforms

Exchanges

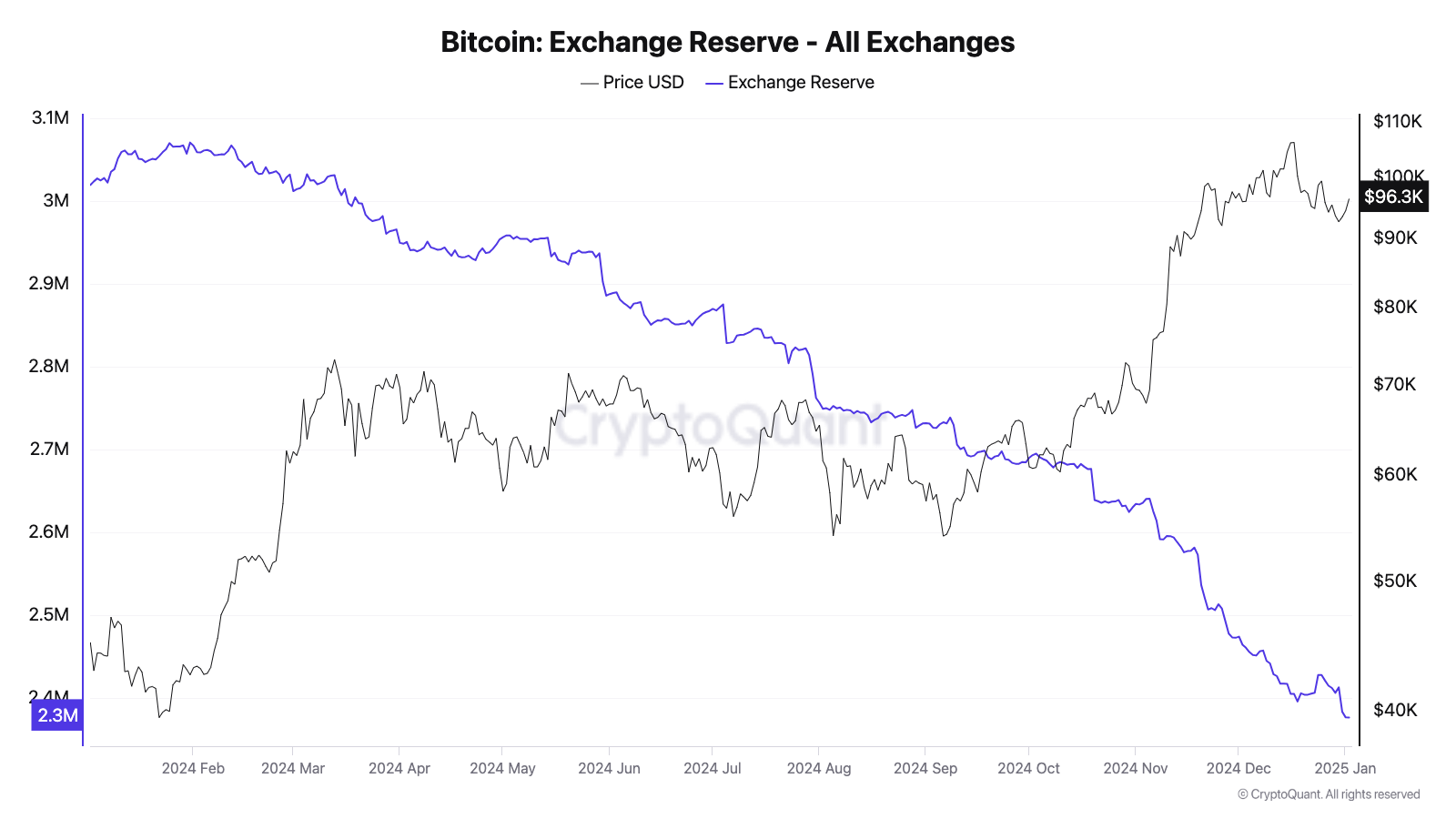

Another popular supply shock indicator is the amount of Bitcoin stored on exchanges and over-the-counter (OTC) platforms, with some observers pointing out that existing reserves are at record low levels. As such, Bitcoin’s exchange reserves experienced a sharp 21% decline in 2024, reaching levels not seen since 2018, according to CryptoQuant. Over 600,000 BTC were withdrawn from major exchanges, with around 40% of these withdrawals occurring after the U.S. elections.

Spot-focused exchanges were the hardest hit, seeing a 31% reduction in their Bitcoin holdings. In contrast, derivatives-oriented platforms fared slightly better, with a 13% decline, most of which occurred in the final quarter of the year.

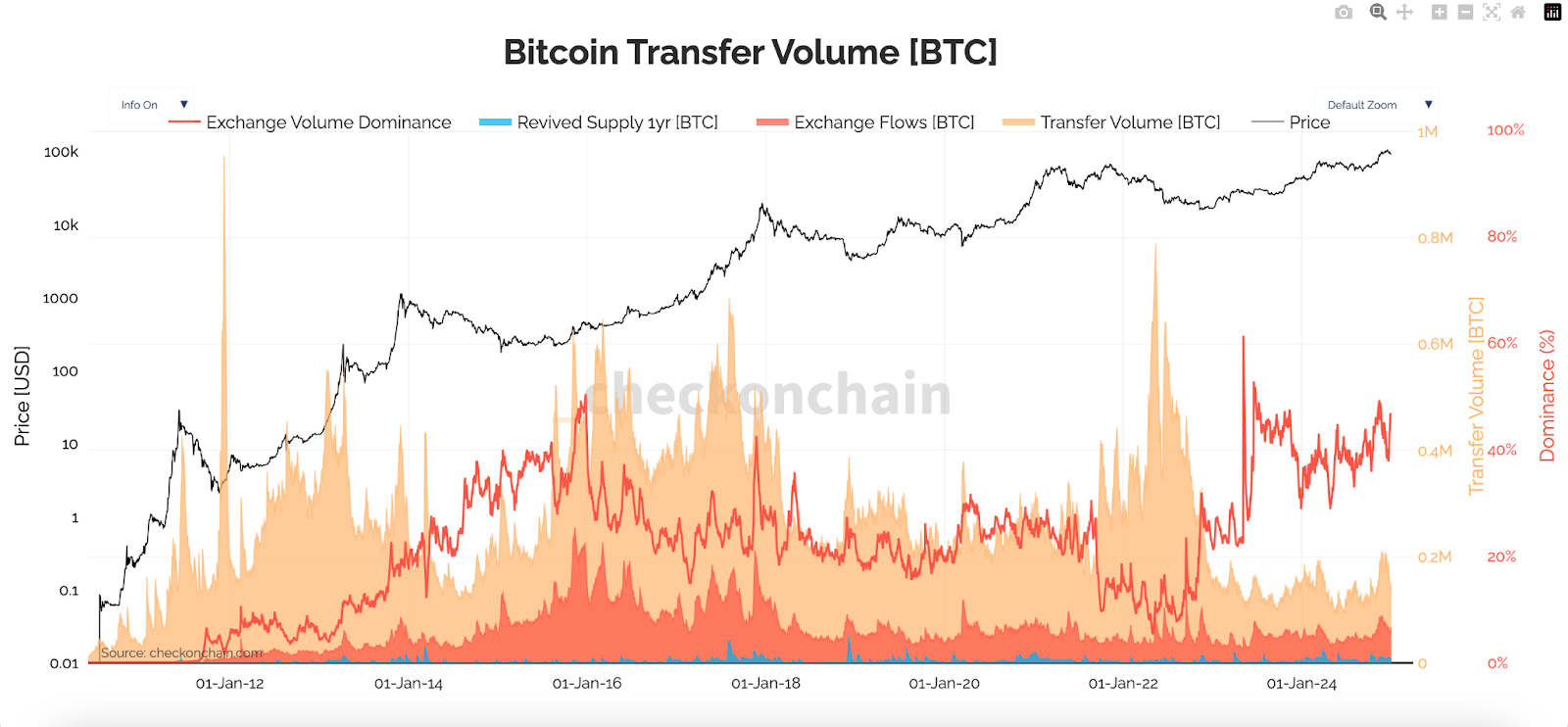

However, BTC-denominated daily exchange-related transfer volumes, including deposits and withdrawals, remained stable at 40,000-80,000 BTC in 2024 — a range consistent since 2018. Stable transfer volumes despite significant withdrawals suggest that holders are moving Bitcoin to cold storage rather than liquidating, signaling long-term confidence. In addition, it highlights steady trading behavior, implying the market remains active and balanced despite reduced exchange reserves.

Approximately 40% of Bitcoin’s transaction volume was linked to exchanges, fluctuating from a local low of 29% in April to a high of 49% in November. While still below the 61% peak of May 2023, this new baseline reflects the enduring influence of exchanges within Bitcoin’s ecosystem, even as OTC platforms gain popularity among institutional investors.

OTC Platforms

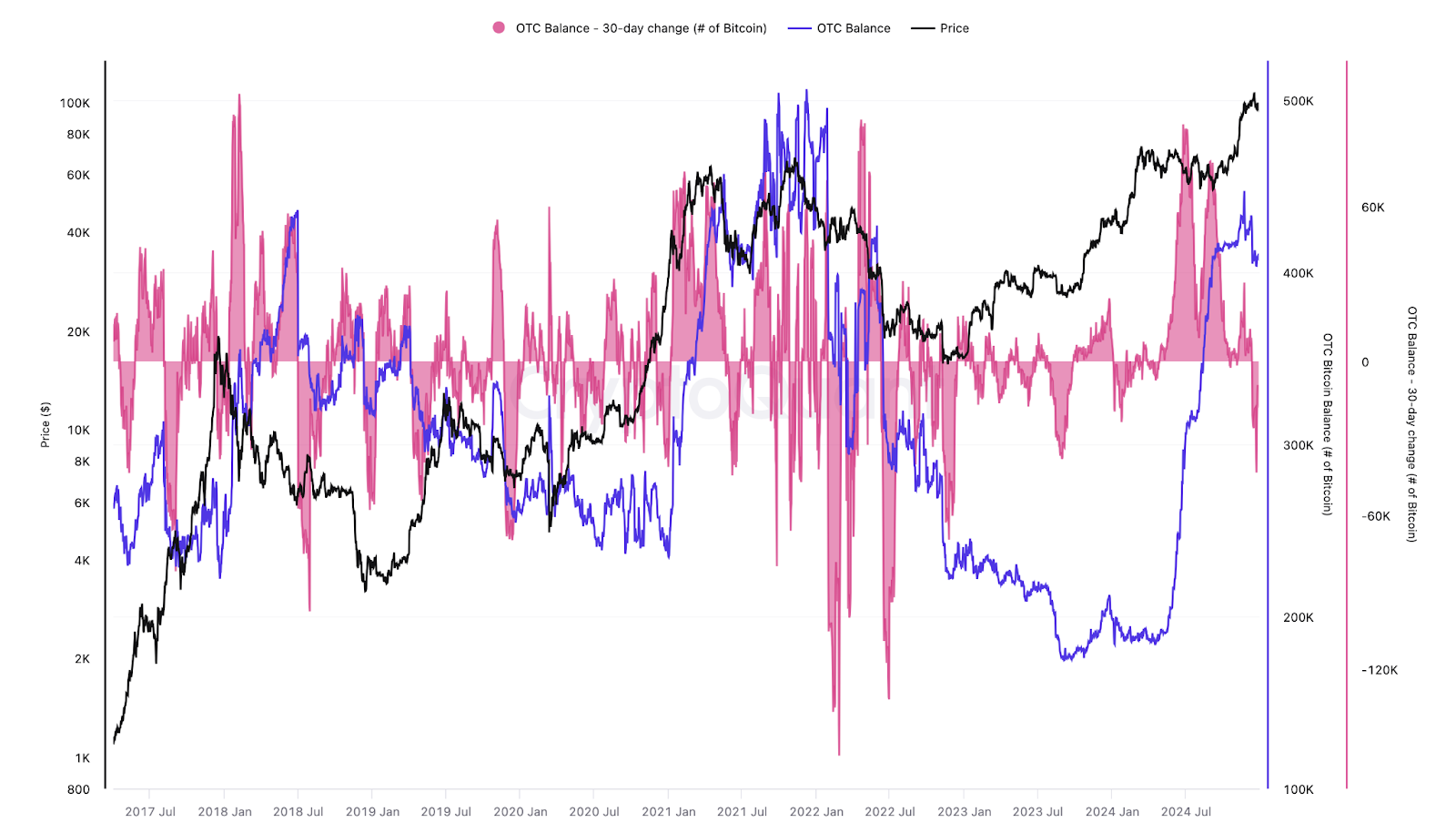

While exchange reserves saw a decline in 2024, OTC platforms accumulated over 208,000 BTC, increasing their balances by 105% year-on-year. As a result, OTC platforms now hold over 400,000 BTC, their highest level since 2022. This increase could signal preparation for higher demand, especially amid increased buying pressure in Q1.

In addition, this dynamic highlights a potential redistribution of supply from exchanges to OTC platforms. This trend not only diversifies the liquidity landscape but also underscores the market’s evolving dynamics as institutional players solidify their presence.

Looking into 2025

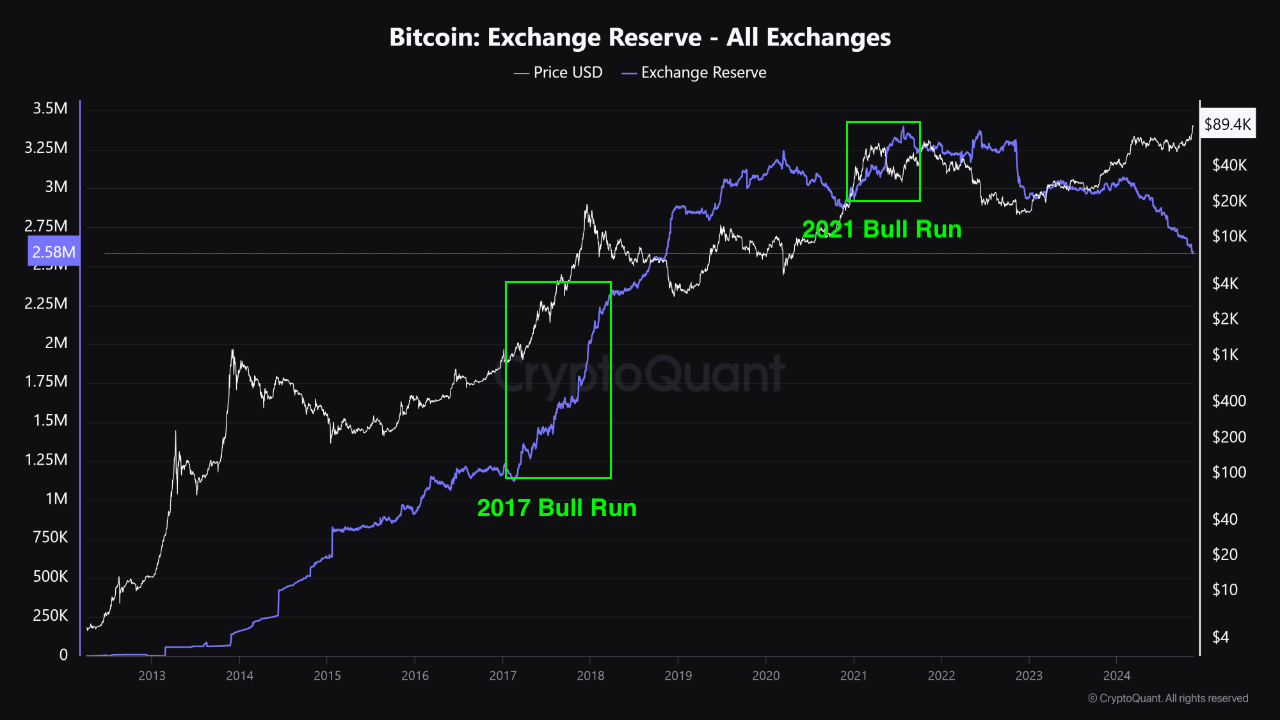

During previous bull runs in 2017 and 2021, both exchange and OTC reserves trended upward alongside increased market activity and revived supply. This historical pattern suggests a potential recurrence in 2025, albeit with a stronger influence from institutional and high-net-worth investors. While the risk of a supply shock remains low for now due to a significant margin of safety on exchanges and OTC platforms, a continued decrease in reserves could amplify upward price movement during this cycle.

Market Depth

Aggregated Market Depth Breakdown

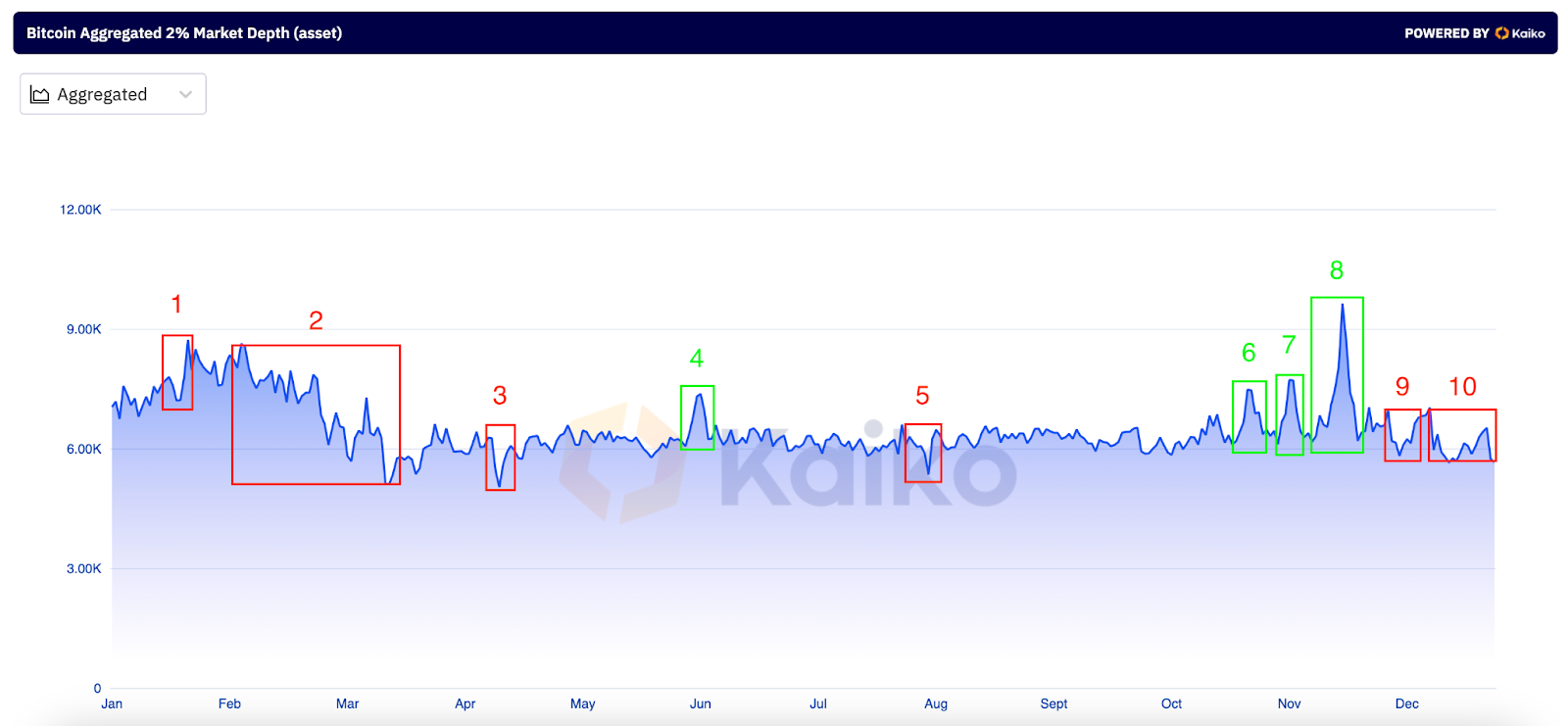

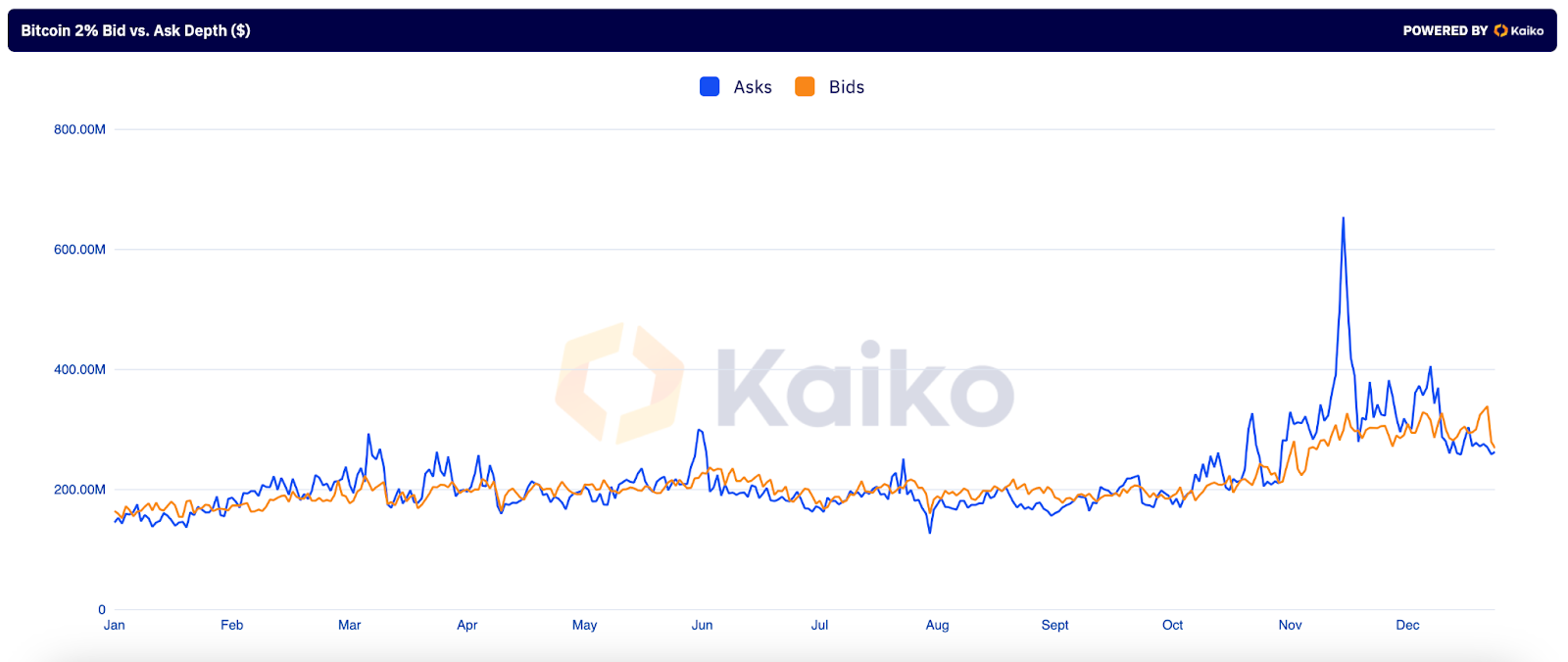

To assess exchanges’ resilience amid record outflows, let’s dive into their liquidity dynamics using the 2% market depth. This metric measures the cumulative volume of bids and asks within 2% of the mid-price, providing a snapshot of liquidity and market stability.

In 2024, the USD-denominated 2% market depth increased by 61%, while the BTC-denominated value decreased by 26%, with a notable drop in Q1 (2). This early-year decline likely stemmed from liquidity reassessments following Bitcoin’s rapid price appreciation, and a shift toward OTC platforms driven by institutional activity.

Local peaks and valleys in market depth can be attributed to several catalysts:

- (1, 9) Altcoin seasons.

- (3) Geopolitical events, such as Israel’s attack on Iran.

- (4, 6) Bitcoin’s rally to challenge an all-time high.

- (5) Yen carry trade unwinding.

- (7) U.S. election results.

- (8) Gary Gensler’s resignation.

- (10) Christmas holidays and/or Bitcoin correction.

Notably, throughout the year, asks exceeded bids approximately 58% of the time, highlighting consistent selling interest. Despite this, buyers aggressively absorbed sell orders, driving price appreciation and signaling a strong accumulation phase. Sellers attempted to capitalize on rising prices, but robust underlying demand prevented a reversal of the bullish trend. The largest disparity between asks and bids occurred in late November, following the announcement of SEC Chair Gary Gensler’s resignation.

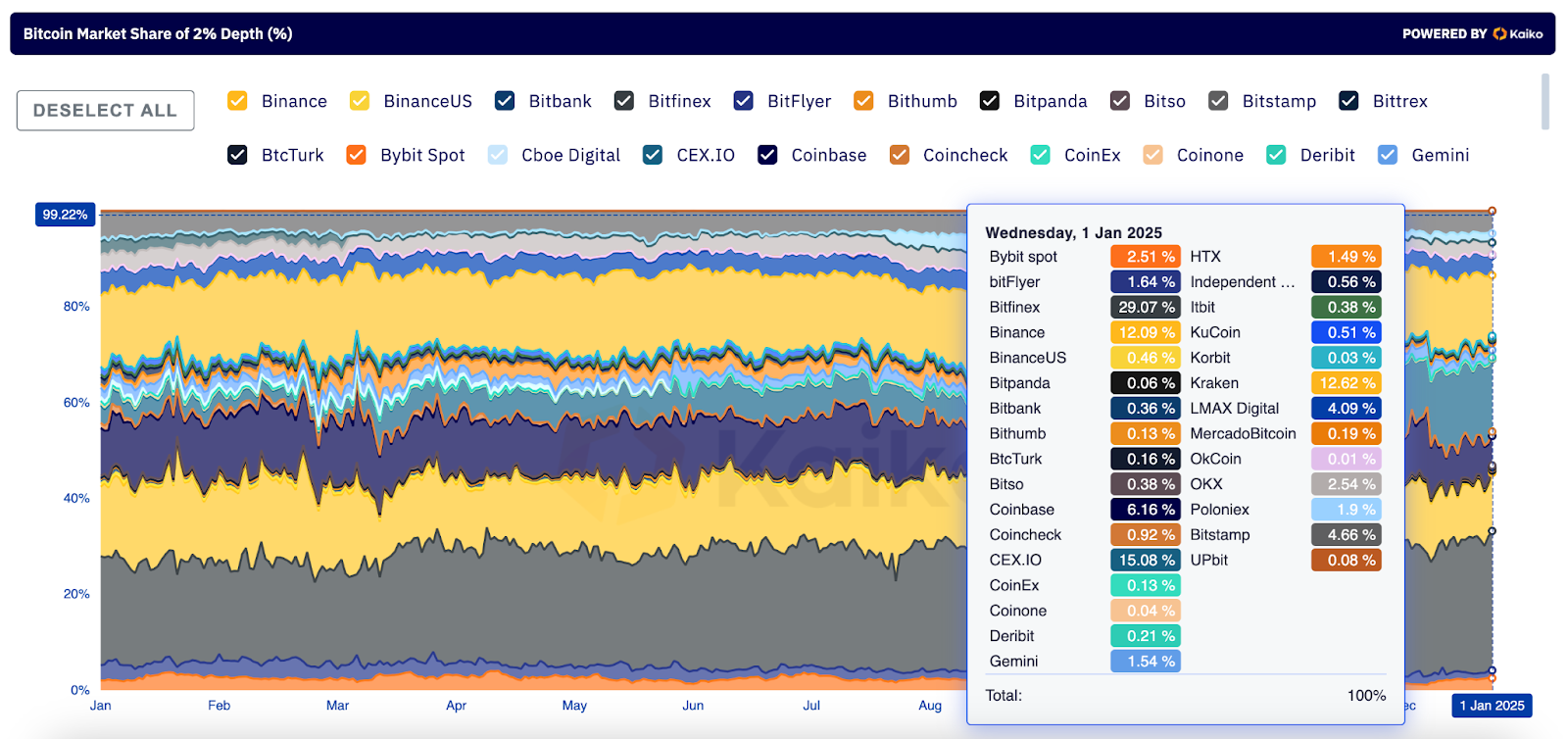

Liquidity Changes Between Exchanges

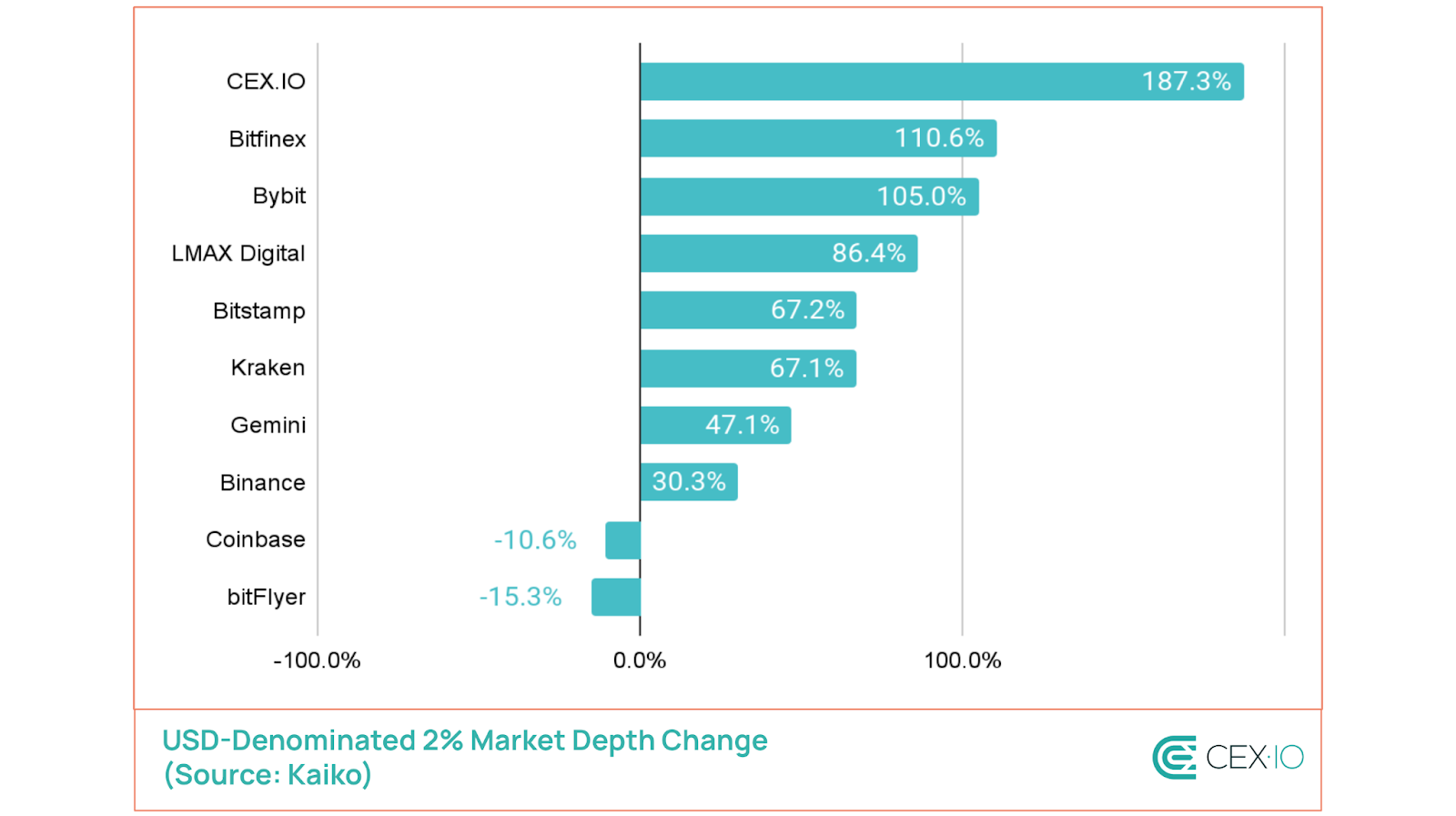

The liquidity landscape across exchanges has also shifted significantly in 2024, with top exchanges consolidating their market share. According to Kaiko data that includes 33 major exchanges, the top three exchanges in terms of 2% market depth now account for 57% of the market, up from 53% at the start of the year. At the time of this writing, these exchanges include Bitfinex, Kraken, and CEX.IO, with the latter quadrupling its market share in 2024.

Notably, since CEX.IO’s trading engine utilizes liquidity aggregated across multiple sources, its market depth increase partially contributed to the rising share of certain exchanges. Much of CEX.IO’s growth occurred in Q4, following an update to its aggregation engine that expanded liquidity sourcing and enabled near-zero spreads on most trading pairs, including Bitcoin.&

Note: The performance from January 1, 2024, to January 1, 2025.

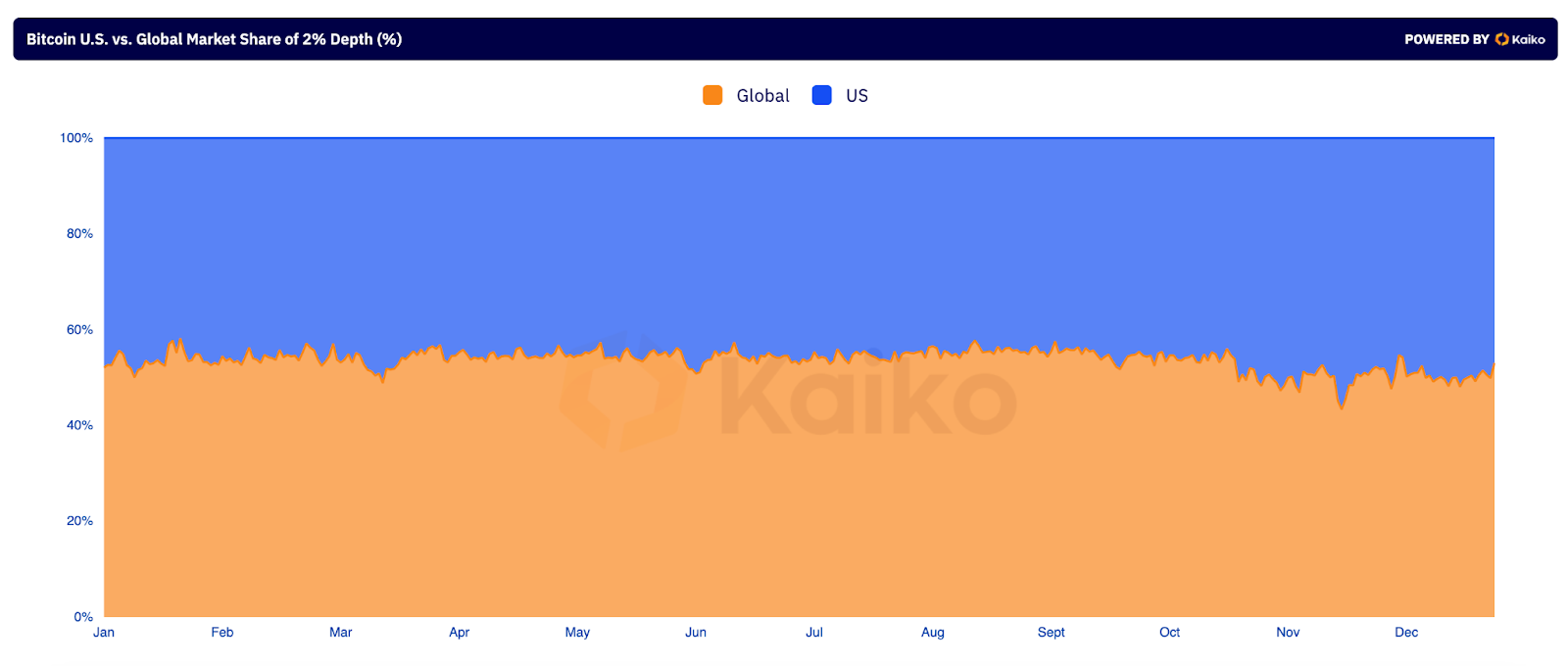

Geographic trends showed that there primarily was a 55/45 parity in market depth between non-U.S. and U.S. exchanges. Following the U.S. elections, U.S. exchanges temporarily dominated market depth, contributing to November’s price rally. Brief spikes in U.S. exchange liquidity were also observed in March, June, and October, coinciding with Bitcoin’s price reaching or approaching all-time highs.

Looking into 2025

When observing liquidity, it’s important to keep in mind that USD-denominated depth remains a key liquidity metric for many traders and institutions. As a result, despite a drop in BTC terms, overall liquidity improved in 2024. This sets up the stage for further enhancement in 2025, as Bitcoin’s cyclic bull runs have been typically associated with increased liquidity.

Larger exchanges are likely to solidify their dominance, building on their recently increased market share. In turn, market depth will likely continue shifting towards U.S. exchanges, as trading becomes increasingly concentrated on U.S. hours.

Conclusion

Although the supply and liquidity developments of 2024 have laid a strong foundation for Bitcoin’s potential upward momentum this year, it appears to be too early to declare the onset of a supercycle, with a massive supply shock and no prolonged bear market. Bitcoin continues to maintain a substantial margin of safety, with millions of BTC poised for sale as market indicators start signaling a potential cycle top. This awaiting supply acts as a natural counterbalance to unbridled optimism, reinforcing the persistence of the 4-year cycle theory. Despite the allure of overbullish expectations, this cyclical framework appears likely to shape Bitcoin’s market dynamics for the foreseeable future.

The web content provided by CEX.IO is for educational purposes only. The information and tools provided neither are, nor should be construed as, an offer, or a solicitation of an offer, or a recommendation, to buy, sell or hold any digital asset or to open a particular account or engage in any specific investment strategy. Digital asset markets are highly volatile and can lead to loss of funds.

The availability of the products, features, and services on the CEX.IO platform is subject to jurisdictional limitations. To understand what products and services are available in your region, please see our list of supported countries and territories. This page includes additional links to information about individual products, and their accessibility.

You can get bonuses upto $100 FREE BONUS when you:

💰 Install these recommended apps:

💲 SocialGood - 100% Crypto Back on Everyday Shopping

💲 xPortal - The DeFi For The Next Billion

💲 CryptoTab Browser - Lightweight, fast, and ready to mine!

💰 Register on these recommended exchanges:

🟡 Binance🟡 Bitfinex🟡 Bitmart🟡 Bittrex🟡 Bitget

🟡 CoinEx🟡 Crypto.com🟡 Gate.io🟡 Huobi🟡 Kucoin.

Comments